))

Episode 37: Episode 37 – Special Session on Property Insurance

Manage episode 327489582 series 3032177

תוכן מסופק על ידי The Florida Insurance Roundup from Lisa Miller & Associates and The Florida Insurance Roundup from Lisa Miller. כל תוכן הפודקאסטים כולל פרקים, גרפיקה ותיאורי פודקאסטים מועלים ומסופקים ישירות על ידי The Florida Insurance Roundup from Lisa Miller & Associates and The Florida Insurance Roundup from Lisa Miller או שותף פלטפורמת הפודקאסט שלהם. אם אתה מאמין שמישהו משתמש ביצירה שלך המוגנת בזכויות יוצרים ללא רשותך, אתה יכול לעקוב אחר התהליך המתואר כאן https://he.player.fm/legal.

The Florida Legislature will meet in a special session May 23-27 called by Governor Ron DeSantis to “bring some sanity and stabilize” Florida’s property insurance market. Homeowners are suffering big rate increases and some have lost their coverage, while a growing number of insurance companies are going insolvent or reducing or eliminating their policy-writing in the state.

Former Florida Deputy Insurance Commissioner Lisa Miller explores the problems in the marketplace with an insurance agency executive and a top real estate agency owner who share their ideas on which reforms would be most effective for lawmakers to achieve.

Show Notes

The Governor’s proclamation calls for the legislature to address property insurance, reinsurance, civil litigation, and changes to the Florida Building Code to improve the affordability and availability of insurance coverage. The legislature failed to pass any reforms in its regular 60-day session earlier this year. Reforms passed into law in its 2021 session under SB 76 have had key roofing solicitation restrictions temporarily enjoined from enforcement by a federal judge.

Ron Assise, Senior Vice President of Horton Personal Insurance, in Estero, Florida, said his clients are experiencing “sticker shock” on their homeowners insurance premiums. “Clients are very disrupted when they get their bill and it's 20% or 25% or 30% more than it was last year,” said Assise, who is part of The Horton Group of Chicago, an insurance, employee benefits and risk advisory firm.

Whitney Dutton, owner of The Dutton Group@Re/Max First, a full-service real estate agency in Fort Lauderdale, said with 30% of his clients from out of state, the sticker shock is even greater and comes with greater consequences, too. “When people get a loan, the lender uses a debt to income ratio in order to qualify them for a purchase. When the debt to income gets offset by $1,000 to $4,000 of swings from insurance quotes, that can really put a damper on someone's ability to purchase a home, or to be competitive when trying to bid on property,” Dutton said. He said some home purchasers have faced being dropped by their insurance company following a quality control check 60-90 days after closing, when it’s determined the roof is too old or other changes are required to keep the policy in force. “A third way that it comes is simply just getting dropped without any notice whatsoever from insolvency due to a lot of these companies that are just getting out of the market,” said Dutton, whose group was the top Realtor in Fort Lauderdale in total transactions last year.

Rising Litigation: The Governor’s proclamation states upfront that “Florida’s general tort environment related to property insurance has led to thousands of frivolous lawsuits…and according to the Office of Insurance Regulation, Florida accounted for 79% of the nation’s homeowners insurance lawsuits while making up only 9% of the nation’s homeowners insurance claims. Florida citizens are seeing the effects of this higher litigation in their rising premiums.”

Assise said litigation reform is a must. “We all know that Florida is far and away the unfortunate leader in litigation when it comes to insurance claims with approximately 116,000 insurance related lawsuits last year versus less than 1,000 for the rest of the country combined,” he said.

Roof Claims: Assise suggested the legislature approve what was in last session’s SB 1728, passed by the Senate but not taken up by the House, which would require a roofing deductible or an actual cash value or repayment schedule for older roofs, in place of the current full replacement value. “Doing that will really make it not worth its while to an attorney to go after an insurance company, if they're going to get, let's say 40 cents on the dollar as an example,” Assise said.

His other suggestions are to change the state’s 25% Roof Repair/Replacement Rule that requires an entire roof be replaced if 25% or more of it is damaged and ease existing material “matching” requirements in repairs, where a new roof is required if the repaired material can’t be matched with the rest of the undamaged roof. “So insurance carriers are paying claims of 25, 30, 40, or $50,000, where the damage might be $1,000. These are the things that need to be addressed to really make a significant difference going forward,” Assise said. “The incentives go away for both the roofers and the trial attorneys that see big dollar signs when it's most likely probably wear and tear or just a plain old older roof where someone should be taking care of the maintenance on their home like any other thing.”

Those proposed restrictions would have to come with a lower policy premium cost, said Dutton, who owns eight rental properties of his own and has seen annual premiums on each grow from about $2,800 per year in 2017 to $4,200 today. “I'm okay with it if the policy cost is relative to that type of coverage, but from what we're seeing in the type of properties that I deal with, they're writing the policies with a lot of those exclusions, water damage, restoration, and they're not changing the price of them,” Dutton said. “The lower coverage isn't what people are worried about. It's the cost…and it’s being passed on unfortunately to the renters.”

While Assise said he can appreciate consumers wanting something substantial in return for giving up some coverage, the cost break won’t be immediate. “There's so much red ink going out at this point, it’s difficult for that to happen without these legislative changes where they can see light at the end of the tunnel and the reinsurance industry can see light at the end of the tunnel, which very much affects the pricing for the insurance carriers in Florida,” said Assise, a 40-year veteran of the industry and both a Certified Insurance Counselor and Certified Personal Insurance Counselor. The Florida insurance industry has seen two straight years of net underwriting losses exceeding $1 billion each year.

Assignment of Benefits: For Dutton, those restrictions are just “the tip of the iceberg” and what’s also needed is further reform of abusive Assignment of Benefit (AOB) contracts between homeowners and various contractors, roofers, and public adjusters. “A lot of these homeowners don't even know that this stuff is happening. They've simply signed a piece of paper that allows these contractors to act on their behalf. And I know people firsthand, that are shocked what happened and never would have went through it to the level that these different companies have squeezed every dime they can out of the insurance companies, “ Dutton said.

“The three of us realize that the consumer is the loser here,” said host Lisa Miller. “You've got the consumer that's paying the exorbitant premiums. They're trying to buy or afford to stay in their current homes. And then they get locked in by an unscrupulous bad actor at the front door,” she said. She read a text between a roofer and a colleague of hers on a home repair, in which the roofer is coaching the homeowner on how to represent old damage so that insurance covers it, while also offering an unlimited $200 referral for each neighbor who “needs a free roof.”

“The legislature is going to have to understand that this is going to come at a cost to somebody,” said Dutton, “and the attorneys in these larger law firms that this is all they focus on, they're going to take a hit. So the legislators are going to have to have the political courage to stare down some of these big law firms who may donate to certain areas that they're going to have to take a hit. And it's going to have to come from top down, the legislator down,” he said.

Prior to the Governor’s special session call, regulators with the Florida Office of Insurance Regulation and the Florida Building Commission had begun creating regulatory measures to help. They’ve implemented new policy to allow optional roof deductibles, ease existing material “matching” requirements in repairs, and approved mandatory arbitration clauses in insurance policies. They’re also considering further measures, including making exceptions to the state’s 25% Roof Repair/Replacement Rule.

While the Governor’s proclamation did not provide specific proposals for the legislature to consider in the upcoming special session, Miller shared there are two other key issues that will likely be addressed, besides roof claims and litigation reform. They are reform of the state-backed Citizens Property Insurance Corporation, whose legislatively mandated and actuarially unsound rates have contributed to a policy count expected to surpass one million policies by year-end, and allowing insurance companies to access less expensive reinsurance from the Florida Hurricane Catastrophe Fund.

“The Florida Legislature basically left homeowners exposed to a perfect storm of rising rates, limited coverage and diminishing options, because it failed to pass the reforms that should have been passed earlier this year. Let's hope that changes May 23,” said Miller.

Links and Resources Mentioned in this Episode

Governor DeSantis Proclamation of Special Session on Property Insurance (April 26, 2022)

Court Denies Effort to Stop All of SB 76 for now (LMA Newsletter of January 24, 2022)

The Horton Group Agency

The Dutton Group @ RE/MAX First Realty

Calls for a Special Session Falling on Deaf Ears (LMA Newsletter, March 28, 2022)

If You Can’t Legislate, Regulate! (LMA Newsletter, April 11, 2022)

More Insurance Companies in Trouble (LMA Newsletter, April 25, 2022)

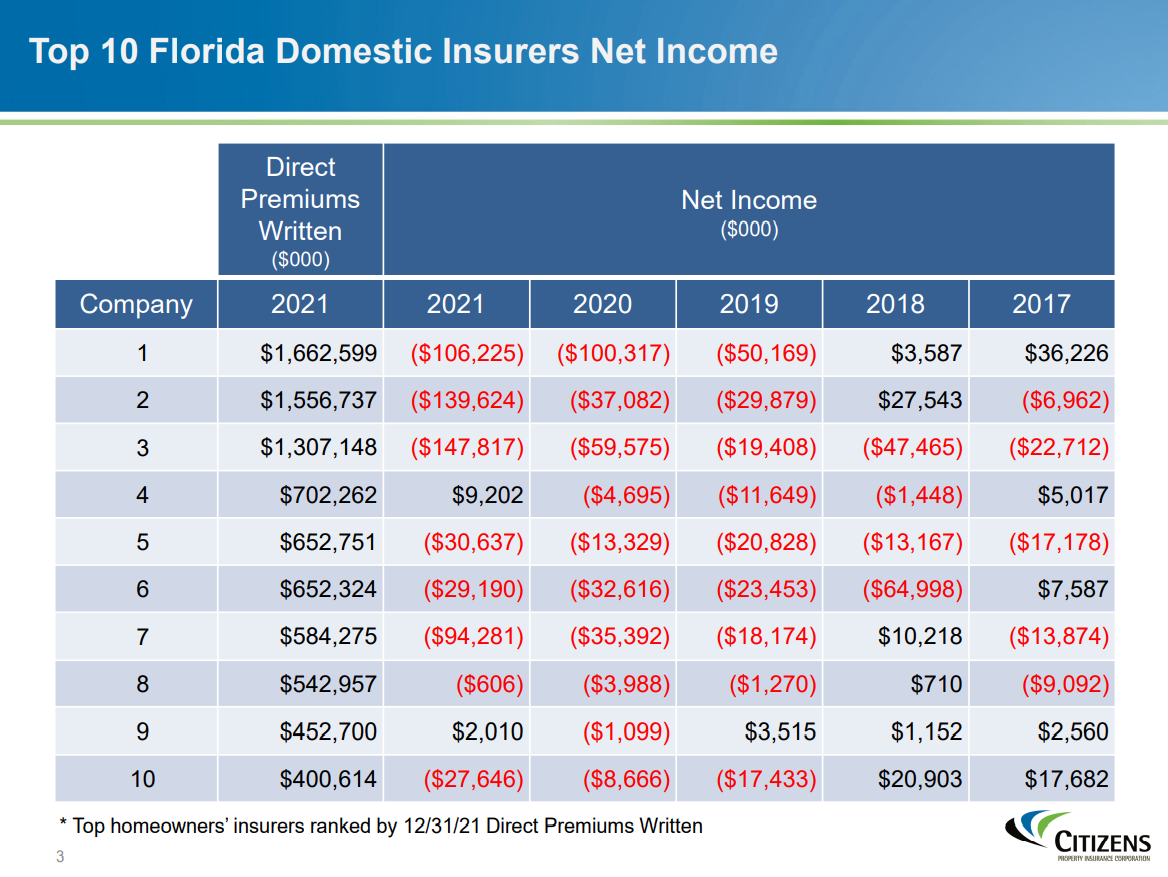

Top 10 Florida Domestic Insurers Net Income Losses (from Citizens Property Insurance Corporation, March 2022)

Citizens Insurance Losing Money (LMA Newsletter, March 28, 2022)

Private Insurance Industry Cumulative Rate Filings 2020-2021 (from Citizens Property Insurance Corporation, March 2022)

“No Roof Left Behind” campaign solicitation pitch (Facebook video advertisement by Roofing and Reconstruction Contractors of America)

Roofers Busted in “Free Roof” Fraud (LMA Newsletter, March 28, 2022)

Unlicensed Adjuster Busted (LMA Newsletter, April 25, 2022)

Repair contractors’ newest billing strategy leaves homeowners on the hook if insurers don’t pay (Sun Sentinel, November 18, 2021)

Demolish Contractor Fraud Webpage (Florida Insurance Consumer Advocate)

Florida Fraud Fighter Reward Program (Florida Department of Financial Services)

First Quarter 2022 Florida Insurance Litigation Statistics (LMA Newsletter of April 11, 2022)

Top 20 Attorneys Filing Property Insurance Lawsuits - 2022 Q1 (Florida Department of Financial Services, April 2022)

Property Insurance Crisis in Florida (WPLG-TV Miami, April 27, 2022)

Insurance defense attorney slams Florida’s ‘egregious’ homeowners insurance system (WFLA-TV Tampa, April 28, 2022)

Major Provisions of SB 76 (2021 Roofing & Litigation Reform law)

Major Provisions of HB 7065 (2019 Assignment of Benefits Reform law)

Assignment of Benefits & Insurance Litigation Webpage (Lisa Miller & Associates)

** The Listener Call-In Line for your recorded questions and comments to air in future episodes is 850-388-8002 or you may send email to LisaMiller@LisaMillerAssociates.com **

The Florida Insurance Roundup from Lisa Miller & Associates, brings you the latest developments in Property & Casualty, Healthcare, Workers' Compensation, and Surplus Lines insurance from around the Sunshine State. Based in the state capital of Tallahassee, Lisa Miller & Associates provides its clients with focused, intelligent, and cost conscious solutions to their business development, government consulting, and public relations needs. On the web at www.LisaMillerAssociates.com or call 850-222-1041. Your questions, comments, and suggestions are welcome! Date of Recording 4/28/2022. Email via info@LisaMillerAssociates.com Composer: www.TeleDirections.com © Copyright 2017-2022 Lisa Miller & Associates, All Rights Reserved

54 פרקים

{kind=link}